|

October marked the beginning of the CFTC’s fiscal year and 50 years of its existence (a mere five years younger than Mariah Carey). The CFTC kept to some of its regular hits too, with more enforcement actions on swap data reporting, wash sales, and fraud and manipulation.

But the big news, is obviously the election next Tuesday. To that end, in the beginning of the month, a U.S. federal appeals court upheld a lower court’s ruling that KalshiEx can offer trading in Political Event Contracts.

End of Month CFTC Enforcement Updates

The CFTC had a busy first month of its new fiscal year on the enforcement front. You can access our summary of the CFTC’s October enforcement actions here.

Of note, on October 1, 2024, the CFTC announced orders filing and settling charges against Barclays Bank PLC ($4 million civil penalty for swap reporting violations) and three SEFs: Tradition SEF LLC ($875,000 civil penalty for SEF Core Principles violations), BGC Derivative Markets, L.P. ($750,000 civil penalty for swap reporting and SEF Core Principles violations), and GFI Swaps Exchange, LLC ($550,000 civil penalty for swap reporting and SEF Core Principles violations).

While these orders drew praise from the Director of Enforcement, Ian McGinley, for the CFTC’s continued focus in holding registrants accountable for violations in these two areas, they also continued to draw sharp criticism from Commissioner Caroline D. Pham in her statements (1, 2) accompanying the CFTC’s press releases announcing the orders. Commissioner Pham has not been shy in expressing her views through dissenting statements regarding orders and other public remarks that the CFTC should reevaluate its regulation by enforcement approach. Specifically, Commissioner Pham again expressed her concern with the CFTC continuing to bring enforcement actions based on technical and operational rules violations that lack any customer harm, financial loss, or fraud, in particular when violations are based on NFA examination findings, which makes the CFTC an outlier among other financial regulators in her view.

Moreover, in her accompanying statements, Commissioner Pham continued to stress the importance of the CFTC adopting a clear standard for self-reporting potential violations and cooperation credit that is applied consistently. Commissioner Summer K. Mersinger expressed a similar view about self-reporting and cooperation credit in prepared remarks that she delivered during the International Swaps and Derivatives Association’s Annual Legal Forum on October 30, 2024. Specifically, Commissioner Mersinger stated that firms should be eligible for self-reporting credit for reporting to one of the CFTC’s oversight divisions, not just for self-reporting to the Division of Enforcement under the current policy, and firms should be eligible for more than just a reduced fine if they self-report, substantially cooperate, and appropriately remediate, because a firm undertaking all of those actions “has essentially performed many of the CFTC's functions.”

In her recent remarks, Commissioner Mersinger also criticized the CFTC’s perceived focus on the volume of enforcement cases over improving its regulatory oversight and education of market participants. Finally, Commissioner Mersinger criticized the CFTC’s push to resolve enforcement matters before the end of the fiscal year each September. While she noted that this push incentivizes potential respondents to wait until the end of the year to hopefully draw less public attention by being one of many cases announced, it also reduces the time for the staff to make decisions and therefore “increases the risk of promulgating faulty interpretations of the CEA and CFTC regulations.”

Tiffany Payne & Yiran Jiang | Email

Political Event Contracts

When I’m not busy reviewing ISDAs or financial regulations, I am passionate about history and sports (Roll Tide!..tough year). While I have bet on sports (responsibly of course), I have never bet on the outcome of potentially historic events. Contracts on those potentially historical events (event contracts) are considered “excluded commodities”. In 2012, the CFTC issued an order prohibiting the North American Derivatives Exchange (NADEX) from offering “Political Event Contracts” under the CFTC’s then new authority in Section 5c(c)(5)(C)(i) of the Commodity Exchange Act (CEA), which authorizes the CFTC to prohibit an event contract in certain excluded commodities when it is “contrary to the public interest.”

Why would the CFTC ever consider such a prohibition you may wonder? In 2003, the Pentagon’s Defense Advanced Research Projects Agency (yes, “DARPA”) was forced by lawmakers to scrap plans for a futures market to predict political unrest in the Middle East. Lawmakers later used the Dodd-Frank Act to update the CEA to grant the CFTC authority to prohibit such contracts.

Flash forward to June 2023, when the CFTC announced their review under 17 CFR 40.11 of KalshiEx LLC’s “Congressional Control Contracts”. In September 2023, the CFTC’s review was complete and the CFTC denied KalshiEx’s ability to list the Congressional Control Contracts. KalshiEx promptly filed a lawsuit that November. You may also recall that in June of this year, the CFTC issued a proposed rulemaking to align relevant parts of the CEA with regulations and to make technical amendments to the regulation to enhance clarity with regard to excluded commodities.

Well, on October 2, through a series of proceedings and filings, a US appeals court for the D.C. Circuit upheld a lower court’s ruling permitting KalshiEx to list Political Event Contracts. The appeals court held that the CFTC gave “no concrete” basis for how the Political Event Contracts that KalshiEx offers would be against the public interest (the CFTC lost a similar fight against PredictIt). Robinhood has also entered into this market and it will begin offering Political Event Contracts.

In other closely related developments here, on October 4, the CFTC issued staff letter 24-15 extending CFTC No-Action Letter 21-11, which provided relief to KalshiEX LLC, Kalshi Klear LLC, or their participants for failure to comply with certain swap-related recordkeeping requirements and for failure to report to swap data repositories data associated with binary option transactions executed on or subject to the rules of KalshiEX LLC and cleared through Kalshi Klear LLC, subject to the terms and conditions in the no-action letter.

Barrett Morris | Email

Synthetic Risk Transfers

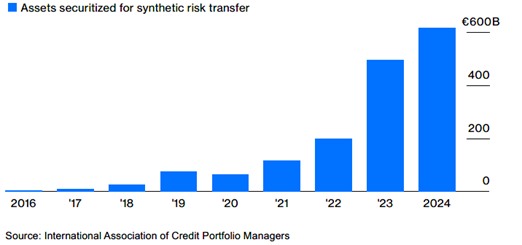

Last February we sent out an update on credit/synthetic risk transfers (SRTs) explaining the structure and how they can provide relief under a bank’s capital rules and off load some risk of loss on relevant loans. Since then, BPI also put out a fantastic one-pager on SRTs, which you can read here.

The Bloomberg Editorial Board recently put out an article claiming that SRTs will essentially be the cause of the next financial crisis. Banks are increasingly using SRTs to transfer credit risk from loans to outside investors, i.e., private credit firms, helping them manage regulatory capital more efficiently.

As you can see from the chart above, which is in the Bloomberg article, SRTs are growing quickly. SRTs, often implemented through credit-linked notes (CLNs) or credit default swaps (CDS), enable banks to retain their loan portfolios while shifting some credit risk to investors. CLNs, sold to multiple investors, reduce repayment obligations if losses occur, and carry minimal counterparty risk; CDS, usually single-investor agreements, function similarly but can be more expensive. Regulatory incentives for SRTs allow banks to lower capital requirements, freeing resources for other lending activities.

However, CLNs are unsecured bank debt that depend on the performance of underlying collateral, allowing banks to mitigate risk while retaining client relationships. The primary investors in SRTs are private credit funds, which maintain lower leverage than banks and are likely well-positioned to absorb potential losses.

The Bloomberg article says that regulators are “oblivious” to what the authors perceive as a risk. Notably, last year the Federal Reserve provided guidelines for banks directly issuing CLNs, requiring individual approval from the Federal Reserve based on transaction details.

Yiran Jiang | Email

Voluntary Carbon Credits Continued

In last month’s “The Desk” we brought you an update on new CFTC guidance concerning VCCs, which was targeted towards DCMs, but should really be considered across all market participants. Well since then, October marked the issuance of the very first VCC enforcement action against a VCC project developer who was, among other things, submitting false data to a carbon credit registry and ultimately misleading participants as to the amount of carbon credits the VCC was creating. We wrote up a complete summary of the guidance and enforcement action in a piece that was published in WestLaw and can be found here.

Barrett Morris & Jules Carter | Email

Proposed Changes to FX Global Code

On October 9, the Global Foreign Exchange Committee (GFXC) issued a request for feedback on proposed amendments to the FX Global Code and disclosure cover sheet amendments. In case you’re unaware or just don’t trade FX products, the FX Global Code (last updated in 2021) is a set of industry guidelines designed to create a fair and transparent FX marketplace. The consultation period for comments was seemingly short and ended on October 25.

The proposed amendments to the FX Global Code are centered on elements of FX settlement risk and netting under Principles 35, 50 and 51. According to the GFXC, these amendments are designed to improve guidance on FX settlement risk mitigation practices and clarify that all market participants have a responsibility for reducing FX settlement risk.

The proposed changes to the Liquidity Provider Disclosure Cover Sheet and the Platform Disclosure Cover Sheet highlight changes to (1) how Market Participants disclose their use of FX data derived from client interactions with third parties and (2) disclosures concerning FX order handling that comports with a transparent order execution policy.

The Foreign Exchange Professions Association (FXPA) replied to the proposed changes citing the short comment period and what they understand to be “overly prescriptive” updates that deviate form the FX Global Code’s principal-based approach. Further the FXPA wrote to the GFXC that the proposed updates “lack the necessary background or rationale explaining the proposed amendments.” If the amendments are drafted as is, the FXPA believes there could be unintended consequences.

Barrett Morris | Email

Other interesting October reads:

|